Power Cut? How the EU Is Pulling the Plug on Electricity Markets

24 December 2015

SUGGESTED

Research

Lifestyle Economics

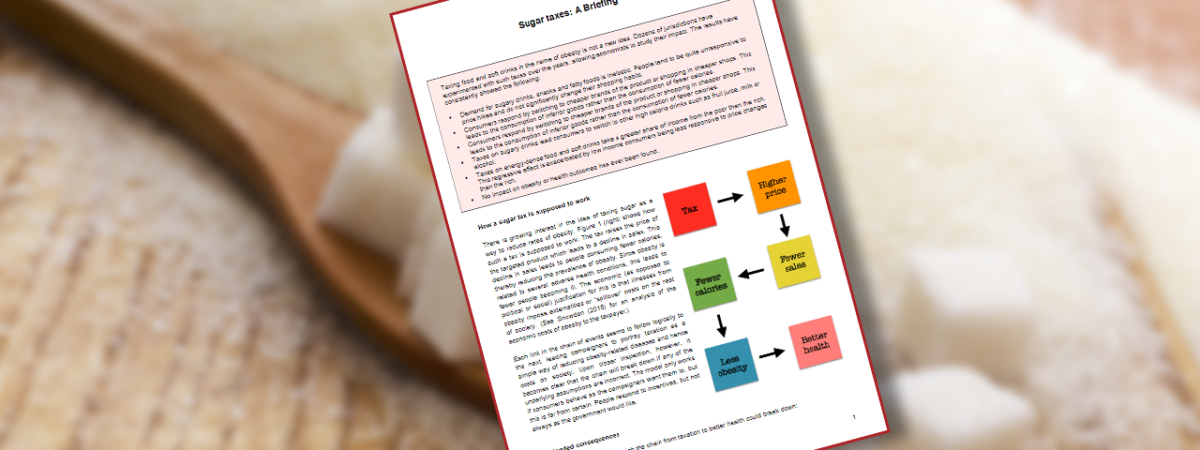

New IEA briefing explains why a sugar tax would be regressive & wrong

13 January 2016

Tax and Fiscal Policy

19 November 2024

Don't let the lights go out at Christmas - EU policies hampering UK electricity market

To purchase a copy of Power Cut? How the EU is Pulling the Plug on Electricity Markets at £15 each, click here For orders of five or more copies, please email reception@iea.org.uk to discuss discounts

Summary:

The paper featured in The Daily Mail.

To read the press release, click here

Hobart Paperback 180

Fullscreen Mode

Summary:

- Technical features of the electricity industry, together with the ideological climate that prevailed after World War II, led to nationalisation. Over time, it became clear that the arguments for nationalisation were unconvincing. Firstly, changes in technology led to the ability to produce electricity on a smaller scale. Secondly, it became clear that, even if some parts of the process of electricity production and distribution had ‘natural monopoly’ aspects, other parts did not. Moreover, it became increasingly understood that state electricity suppliers were very inefficient.

- The UK led the way when it came to reform. Markets were deregulated, competition was promoted and the industry was privatised. There was then price-cap regulation of the natural monopoly element. From 1990 to 1999, electricity charges for domestic consumers fell by 26 per cent, with a larger fall for industrial users. Electricity companies were able to use cheaper fuels, free from political constraints. It was not only energy prices that fell in the UK after liberalisation; energy-related greenhouse gas emissions fell by 12 per cent between 1990 and 2010, and emissions per unit of GDP fell by 45 per cent.

- There have been a number of attempts, through EU directives that followed the British model to some extent, to liberalise electricity markets in the EU more generally. By 2007, all EU member states had third-party access (TPA) to electricity networks, and most had transparent wholesale markets and a degree of consumer choice. As a result, the average market share of incumbent dominant firms in the EU fell from 64.9 per cent in 1999 to 55.9 per cent in 2010. Several private and foreign companies also entered markets that had previously been state monopolies. However, these steps were also accompanied by harmonisation and centralisation of regulation at the EU level.

- Around ten years ago, there began a major policy U-turn in the UK. Steps that have reduced competition and the degree of liberalisation include limiting the number of offers and tariffs that suppliers can make to residential consumers, measures that direct electricity generating companies towards particular technologies and long-term agreements to fix prices in markets (such as the agreement with the Chinese government in relation to nuclear energy that guarantees a price about twice the current wholesale price of electricity). These measures will crowd out non-subsidised investments in which the taxpayer does not bear the risk.

- The British U-turn was paralleled by a push from the EU as well as member states towards interventionist climate policies. For example, there are often capital subsidies or tax breaks to install renewable capacity, direct subsidies for renewable energy and feed-in tariffs, which treat renewable generation very favourably. In addition, member states have to grant either priority access or guaranteed access to the grid for ‘green’ electricity. These policies have many detrimental effects. For example, when the demand for electricity falls – as it did post-2008 – renewable energy producers are immune to the consequences. Also, subsidies vary hugely across different technologies and different countries. Photovoltaics received an average subsidy of €496/MWh in the Czech Republic and slightly lower subsidies in Belgium, France, Italy and Luxembourg, whereas biogas and waste received an average subsidy of only €2.76/MWh in Finland. This causes enormous market distortion. To put it simply, for a given cost, the reduction in carbon emissions has been much smaller than if more economically rational mechanisms had been used.

- The cost of reducing CO2 outputs has been huge under EU policies. Even in Finland – the country that has been able to reduce CO2 emissions most cheaply – the cost per tonne of reduced carbon emissions has been around three to five times the value of permits under the EU emissions trading scheme, which provides a proxy for the cost of achieving the decarbonisation goals efficiently. In France, the marginal cost could be around 50 times higher than in Finland. This arises because the compulsory use of national renewables targets means that countries such as Sweden and France are replacing generating capacity that emits very little carbon with renewables. This is hugely wasteful. A carbon tax or cap-and-trade system alone would lead to a much more efficient outcome.

- Further problems caused by climate change policies include the genuinely competitive part of the market being reduced in size and significant supply-and-demand imbalances. Also, the intermittency inherent in many renewable sources of energy leads to price spikes and the potential for either huge increases in consumer prices or blackouts.

- Intermittency has led to pressure for regulated capacity support mechanisms – yet another intervention in the market. These reduce competition further by remunerating electricity producers in a highly regulated environment. Producers are rewarded not for actually producing and distributing power, but for simply having the capacity to do so. Regulatory intervention in this area is not necessary. Where there is the potential for intermittency, market processes are needed to discover whether consumers prefer energy markets to be subject to price spikes and intermittent supply, or whether they prefer a higher average price and more reliable supply and price patterns. Different consumers may have different preferences that can be provided by different companies or tariffs.

- Whilst the latest EU climate change policy may prove to be less expensive than its predecessor, we are a long way from liberalised and efficient energy markets in which CO2 emissions are reduced in the cheapest possible way.

- The UK needs to return to, and the EU to develop, a fully liberalised and competitive energy market. Even if policymakers believe they cannot rely on free markets to correctly price negative externalities from carbon emissions, they should devise policies that supplement markets in internalising the environmental costs of energy production and consumption patterns. This should be combined with liberalisation and the promotion of competition and innovation, both at the wholesale and retail level. The UK experience between 1990 and 2005 showed how successful such policies can be.

The paper featured in The Daily Mail.

To read the press release, click here

Hobart Paperback 180

Fullscreen Mode

SHARE