Beware dodgy forecasts: Aviation markets are a discovery process

5 February 2018

SUGGESTED

Economic Theory

2 February 2018

Healthcare

6 February 2018

Government and Institutions

I suggested in my previous blog on Heathrow that the proposal for a long 3,500m Northwest runway at the airport, included in the draft Airports National Policy Statement, be built in two phases, with the first long enough for short-haul flights (releasing capacity on existing runways for long-haul). There are a number of advantages associated with this proposal, including a less rushed approach to the difficult task of building across the M25 motorway. But how much time could be available for planning and constructing the second phase?

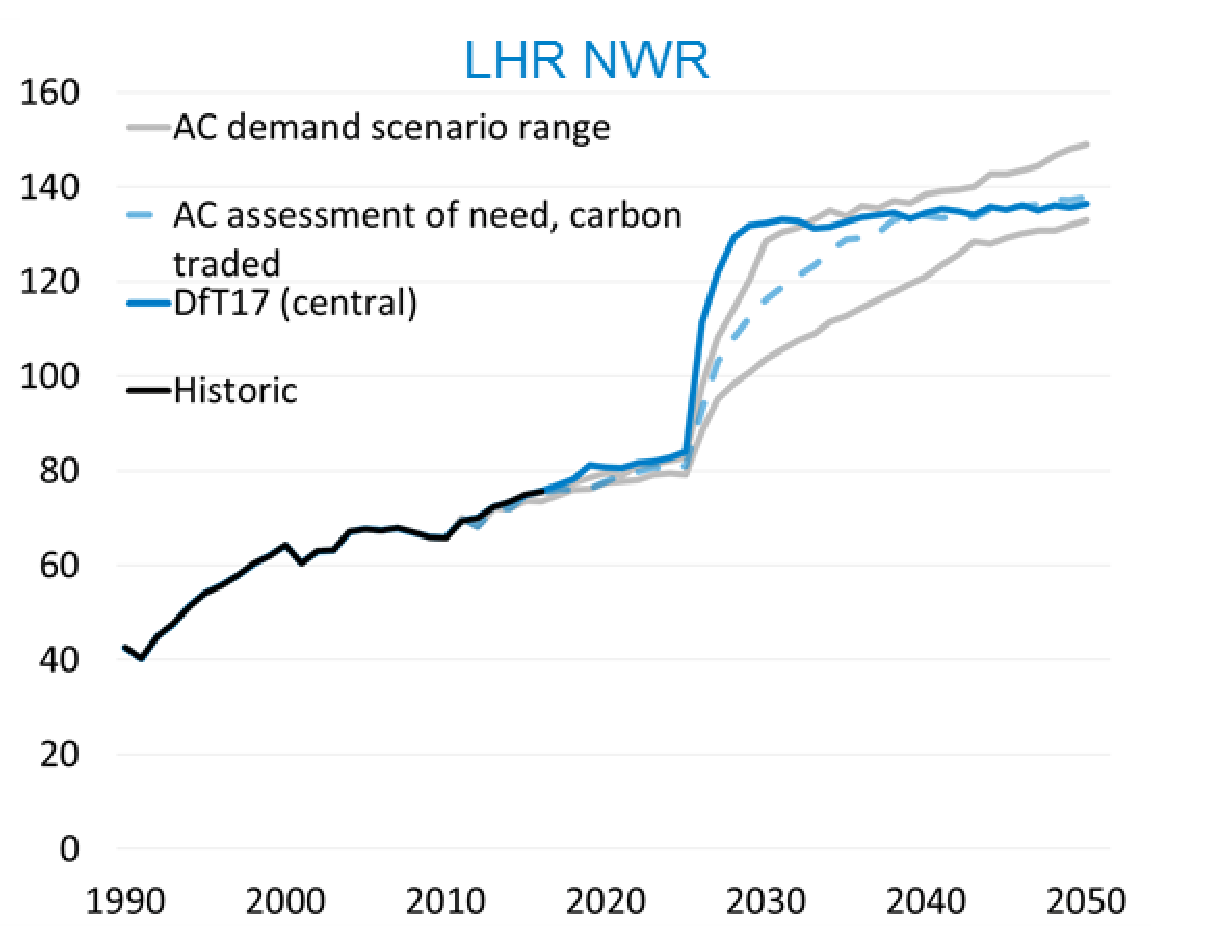

An economist would respond by asking about the profile of incremental costs and benefits for different opening dates. Airport planners, on the other hand, would say that the time available depends upon whether runway capacity is still stressed once a first phase is up and running; in other words, what are the official forecasts for Heathrow’s use in the latter half of the next decade? The short answer is: astonishing.

The solid blue line in the figure shows the Department for Transport’s latest central forecast of passenger demand (in millions per annum) for Heathrow with a Northwest runway. The updated Appraisal Report states that this assumes no phasing of additional capacity and no barriers to airlines making use of this capacity as soon as it becomes available (thus an unconstrained demand). The outcome: more than 50mn annual passengers are added to less than 90mn in the space of little more than two years; “… Heathrow is expected to be full by 2028” (in contrast to the Airports Commission’s date of 2035).

In other words, this forecast is an expectation that Heathrow will add, in an extremely short period, more than the total number of passengers currently using Gatwick (the world’s busiest single runway airport); this borders on a fantasy. Apart from anything else, it is extremely doubtful that air traffic control and the slot co-ordination process could assimilate, in such a very short period of time, the huge increase in flight numbers implied by these passenger figures. It is also difficult to conceive how in the time available airlines could arrange their own affairs: executing the switch of capacity from other markets or obtaining additional aircraft and crew, planning fleet dispositions and marketing new routes and services. It also, incidentally, cuts across the latest proposal of Heathrow Airport Limited to cut construction costs by phasing the introduction of new terminal capacity.

Moreover, the expectation is based on a false economic premise. At the moment there is huge suppressed demand to enter the Heathrow market, a demand fuelled by the prospect of getting a slice of the scarcity rents as a result of the premium fares passengers pay on average for Heathrow flights. Indeed, the Government’s economic appraisal for the scheme is based primarily on the benefits that flow to passengers as a result of the increased airline competition driving down fares (and eliminating rents), at least in the short term. And yet, with fare premiums gone, or more practically, their gradual elimination, will airlines be as keen as they now are to enter the market?

There might be an initial rush of applicants, based on the prospect of first-mover advantage but, as profits are whittled away, nothing like the volumes implied by the Department’s short term forecasts. Also for airlines Heathrow is an expensive airport to use and there is little prospect of airline user charges falling after expansion; the aim now is to try to keep charges close to existing levels. Cost factors and the complexity of operating at Heathrow make it a less attractive proposition for low cost airlines.

The nub of the matter is that aviation markets, in contrast to their portrayal in the Aviation National Policy Statement, are dynamic and, of course, very much a process of discovery. Many routes and services come and go over time. Consequently, the demand equilibrium in a post-Third runway world of reducing scarcity rents at Heathrow remains to be discovered. With rents going or gone will all those prospective long-haul routes to China and elsewhere materialise? And how will hub airports on the Continent react to increased Heathrow competition?

To plan and construct that runway extension across the M25 a leisurely approach will be more than adequate.

An economist would respond by asking about the profile of incremental costs and benefits for different opening dates. Airport planners, on the other hand, would say that the time available depends upon whether runway capacity is still stressed once a first phase is up and running; in other words, what are the official forecasts for Heathrow’s use in the latter half of the next decade? The short answer is: astonishing.

The solid blue line in the figure shows the Department for Transport’s latest central forecast of passenger demand (in millions per annum) for Heathrow with a Northwest runway. The updated Appraisal Report states that this assumes no phasing of additional capacity and no barriers to airlines making use of this capacity as soon as it becomes available (thus an unconstrained demand). The outcome: more than 50mn annual passengers are added to less than 90mn in the space of little more than two years; “… Heathrow is expected to be full by 2028” (in contrast to the Airports Commission’s date of 2035).

-Department for Transport

In other words, this forecast is an expectation that Heathrow will add, in an extremely short period, more than the total number of passengers currently using Gatwick (the world’s busiest single runway airport); this borders on a fantasy. Apart from anything else, it is extremely doubtful that air traffic control and the slot co-ordination process could assimilate, in such a very short period of time, the huge increase in flight numbers implied by these passenger figures. It is also difficult to conceive how in the time available airlines could arrange their own affairs: executing the switch of capacity from other markets or obtaining additional aircraft and crew, planning fleet dispositions and marketing new routes and services. It also, incidentally, cuts across the latest proposal of Heathrow Airport Limited to cut construction costs by phasing the introduction of new terminal capacity.

Moreover, the expectation is based on a false economic premise. At the moment there is huge suppressed demand to enter the Heathrow market, a demand fuelled by the prospect of getting a slice of the scarcity rents as a result of the premium fares passengers pay on average for Heathrow flights. Indeed, the Government’s economic appraisal for the scheme is based primarily on the benefits that flow to passengers as a result of the increased airline competition driving down fares (and eliminating rents), at least in the short term. And yet, with fare premiums gone, or more practically, their gradual elimination, will airlines be as keen as they now are to enter the market?

There might be an initial rush of applicants, based on the prospect of first-mover advantage but, as profits are whittled away, nothing like the volumes implied by the Department’s short term forecasts. Also for airlines Heathrow is an expensive airport to use and there is little prospect of airline user charges falling after expansion; the aim now is to try to keep charges close to existing levels. Cost factors and the complexity of operating at Heathrow make it a less attractive proposition for low cost airlines.

The nub of the matter is that aviation markets, in contrast to their portrayal in the Aviation National Policy Statement, are dynamic and, of course, very much a process of discovery. Many routes and services come and go over time. Consequently, the demand equilibrium in a post-Third runway world of reducing scarcity rents at Heathrow remains to be discovered. With rents going or gone will all those prospective long-haul routes to China and elsewhere materialise? And how will hub airports on the Continent react to increased Heathrow competition?

To plan and construct that runway extension across the M25 a leisurely approach will be more than adequate.

SHARE